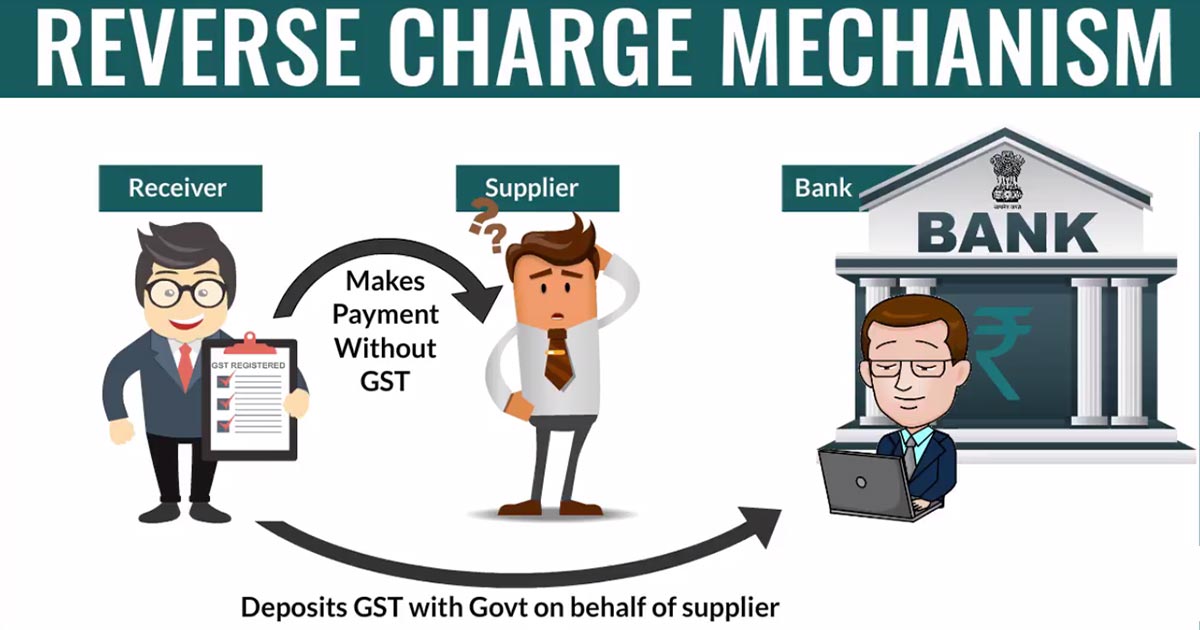

Reverse charge is a mechanism where the recipient of the goods or services is liable to pay Goods and Services Tax (GST) instead of the supplier. Typically, the supplier pays the tax on supply, but under the reverse charge mechanism, the recipient becomes liable to pay the tax, effectively reversing the chargeability.

Objective: The objective of shifting the burden of GST payments to the recipient is to widen the scope of levy of tax on various unorganized sectors, to exempt specific classes of suppliers, and to tax the import of services (since the supplier is based outside India).

Applicability:

- Section 9(3), 9(4), and 9(5) of Central GST and State GST Acts govern the reverse charge scenarios for intrastate and inter-state transactions.

- Different scenarios where reverse charge applies: A. Supply of certain goods and services specified by the CBIC. B. Supply from an unregistered dealer to a registered dealer. C. Supply of services through an e-commerce operator.

Time of Supply Under RCM:

- Time of supply in case of goods: Earliest of the date of receipt of goods, payment, or 30 days from the date of issue of invoice.

- Time of supply in case of services: Earliest of the date of payment or 60 days from the date of issue of invoice.

Registration Rules Under RCM:

- Persons liable to pay GST under reverse charge mechanism must compulsorily register under GST, regardless of threshold limits.

Who Should Pay GST Under RCM? The recipient of goods/services should pay GST under RCM, and the supplier must mention in the tax invoice whether tax is payable under RCM.

Input Tax Credit (ITC) Under RCM:

- Supplier cannot take ITC on GST paid under RCM.

- Recipient can avail ITC on GST amount paid under RCM only if goods/services are used for business purposes.

Self Invoicing: Recipients need to issue self-invoices when purchasing from unregistered suppliers falling under reverse charge, as suppliers cannot issue GST-compliant invoices.

Payment Voucher: Recipients liable to pay tax under reverse charge must issue a payment voucher at the time of making payment to the supplier, as per section 31(3)(g).

This information provides a comprehensive understanding of the Reverse Charge Mechanism (RCM) under GST, including its objectives, applicability, time of supply, registration rules, ITC, self-invoicing, and payment voucher issuance.